The Pell Grant "Trick" to Get a Bigger Tax Refund

IF YOU'RE AN UNDERGRADUATE COLLEGE STUDENT - OR HAVE BEEN ONE IN ANY OF THE LAST THREE CALENDAR YEARS - AND HAVE RECEIVED A PELL GRANT, YOU MAY NOT HAVE GOTTEN AS BIG OF A TAX REFUND AS YOU COULD HAVE.

I'm going to explain how you can categorize your federal pell grants in such a way to leverage the heck out of the American Opportunity Tax Credit. In fact, I used this strategy to file my tax return and amend two previous years' tax returns to get over $1,000 extra dollars back from the IRS than what I got originally.

I've seen other people get over $2,000 back per year in some cases for each year they amended or filed. The sad thing is, they had hired professional tax preparers, who didn't implement this strategy. Ouch.

So let's dive in, and hopefully you'll find that you've left some money on the table that you can reclaim.

A WORD OF CLARIFICATION...

Nothing that I'm about to explain here is shady or underhanded. It's perfectly legal (funnily enough, the IRS taught it to me, as I'll explain below). That's what tax planning and tax strategy is all about - leveraging knowledge of the tax code to pay less taxes. Those who don't understand the tax code pay more tax. Those who do understand the tax code keep more of their money.

So let's get started. If you know how income taxes are calculated - gross income, AGI, taxable income, deductions, credits, and all that - you can skip to the next section.

If you need a quick reminder summary on how your federal income taxes are calculated, here's a pretty good conceptual overview.

THE AMERICAN OPPORTUNITY TAX CREDIT

The American Opportunity Tax Credit is the most generous tax credit for education. It gives you a credit for 100% of the first $2,000 and 25% of the second $2,000 of "qualified education expenses paid" per eligible student. Qualified education expenses, for the most part, are tuition, fees, and any other course materials or supplies that are mandated or required by your institution or the courses you're in.

Eligible student criteria:

You can't have finished four years of college already

You can't claim the AOTC more than four times

You have to be at least a half-time student as defined by your academic institution (which must be "legit" as well)

You can't be a convicted felon for possessing or distributing controlled substances.

OKAY! Enough of the legalese. Just gotta be sure I don't misstate stuff like that.

A QUICK RUNDOWN ON PELL GRANTS

Next, let's go over pell grants briefly, since the whole point of this post is only relevant if you've received one.

A Federal Pell Grant is simply a subsidy - free money - you can get to help pay for undergraduate college education (Pell is just the name of the dude in the Senate who originated the idea). You apply for it on your FAFSA application.

The amount of pell grant you can be awarded is mostly based on your income level. That means if your parents or grandparents are paying for your education, you may not be eligible for it because it will be based on their income. You're more likely to be a pell grant recipient if you're getting through college on your own financially because your annual income probably isn't that high.

The higher your income is, the lower your pell grant award amount, and vice versa. If your income level is over a certain threshold, of course, you don't get any. The max annual pell grant possible through the 2018-2019 school year is $5,920.

HOW SCHOLARSHIPS AND PELL GRANTS ARE ENTERED BY MOST PEOPLE ON THEIR TAX RETURN

Generally speaking, scholarships or grant money you get to pay for higher education expenses are tax free. They aren't taxed as income to the extent that:

It's actually used on qualified education expenses, and doesn't exceed your qualified education expenses

It isn't specifically named for "other purposes", and doesn't say that it can't be used for tuition or fees (a room & board scholarship, for example, would not be tax-free)

It doesn't require you to work or provide services for it - for example, a fellowship or Federal Work Study job on campus

So basically, any scholarship you get that is used to pay qualified expenses is tax-free. Makes sense right? Sounds like the right thing to do on your tax return - "if I don't count it as income, then it will be tax-free and I won't have a higher tax bill."

There's just one caveat to tax-free grants and scholarships. Whatever qualified education expenses you had that were paid for by a tax-free grant or scholarship, you cannot claim a tax credit on those expenses.

If you understand how taxes are calculated, you may be catching on to where I'm going. The thing about tax credits are that tax credits are more valuable than tax deductions. And basically, when you count a scholarship or grant as tax-free income, it's kind of like a deduction, because you're acknowledging to the IRS because you got money (add it to income), but then you count it as tax-free so they let you deduct it and not be taxed on it (subtract it back out again from income).

So here's a grand idea. How about you...

INTENTIONALLY INCLUDE YOUR SCHOLARSHIP IN YOUR GROSS INCOME

No, I'm not crazy (at least not about this). You can actually get more money back on your tax return in some cases if you choose to count your scholarship as income and get taxed on it. Why is that?

On a fine winter evening a few years ago while preparing my own tax return, I was browsing the 97-page IRS Publication 970 on "Tax Benefits for Education" (...don't make fun of me) and came across this little "TIP" box on page 14:

You may be able to increase the combined value of an education credit and certain educational assistance if the student includes some or all of the educational assistance in income in the year it is received.

Hey WHAAA? My tax-brain could not handle the greatness of that statement. What this meant was that you could choose to get taxed on your scholarship, only to turn around and claim a huge tax credit, and therefore, get a tax refund that is more than the extra tax you chose to pay.

Here's how it works:

Basically, if your income level is low enough - which it will be for most college students - adding up to $5,920 of pell grant money to your gross income on your tax return is only going to increase your taxes by $592, because you're only in the 10% marginal tax bracket.

But then, you get to claim up to a whopping $4,000 of qualified education expenses as a tax credit, which can give you up to $2,500 of credit back - 40% of which is refundable.

If that sounded like a bunch of gobbledygook to you, let's run through an example - or rather, a tale. The tale of an extremely likable married couple in college.

THE TAX-SMART PELL GRANT TALE OF JAMES AND PAMELA

Let's take a totally fictional but so seemingly realistic and relatable undergraduate college married couple named James and Pamela - but we'll call them Jim and Pam.

They are both in the middle of undergraduate degrees while working part-time jobs at the same Office under a socially-inept boss. They fit all the requirements to receive the American Opportunity Tax Credit, including saying "NO" to drugs in their youth (you saw the requirement up above). They make $22,000 combined gross income for the year, which gets reported on line 7 of their Form 1040.

They each got a full federal pell grant of $5,815 (this article was written when this was the full pell grant award possible) and for simplicity's sake, let's say that their qualified education expenses added up to that same amount - $5,815 for each of them.

When Pam first prepared their tax return, she read somewhere that the pell grants could be treated as a tax-free scholarship, so she just left it unreported because she figured that those two things just cancelled themselves out. So all she put was $22,000 on line 7 of their tax return:

(Click on images to get a better view)

After that, they get a $12,600 standard deduction for filing "Married, Filing Jointly", a $4,000 exemption for each of them, bringing their taxable income down to only $1,400. Based on the IRS Tax Tables, their total federal income tax bill for the year is only $141 (basically 10% tax rate).

Throughout the year, they had $401 of federal income tax withheld from their paychecks, which was more than their final tax due. So all in all, they looked like they were set to receive $270 back as a tax refund. Not bad - every little bit helps when you're scrimping through school right?

But before Jim and Pam filed their taxes, Pam heard about an awesome blog - *cue shameless plug* - called Wealth Mode and read a post about hacking the tax code to optimize pell grants with the American Opportunity Tax Credit! (sorry, couldn't help myself).

THE PELL GRANT "TRICK"

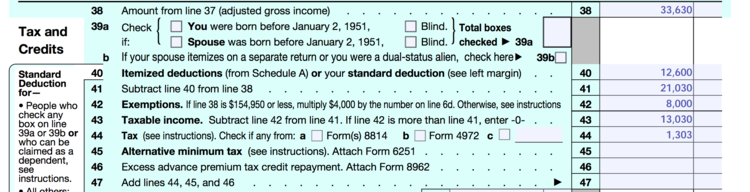

So she started over. First, she decided to intentionally add $11,630 to their gross income, representing the two $5,815 pell grants they got for the year. This brought their total gross income to $33,630. Holy smokes. That seemed like a lot. Pam wasn't sure this was going to work:

After the same standard deduction and exemptions, their taxable income dropped to $13,030, leaving them with a total tax due of $1,303!

But that's when the magic happened. Because Jim and Pam intentionally included their pell grant money as income, they are now allowed to claim the max $4,000 of qualified education expenses for each of them. They had to fill out an extra, annoying worksheet called Form 8863, but as they filled it out, it got interesting - possibly because that worksheet ended up being worth hundreds upon hundreds of dollars (oops, letting the cat out of the bag a bit early).

First, they saw that they had way more than enough qualified education expense to get a nonrefundable credit that wiped out the entire $1,303 tax that they owed:

They stuck that whole credit on the Form 1040, and ended up with $0.

That's already better than what they had, where they were going to owe $141 of tax! Crazy! But then they looked at Form 8863 Part I, which showed their refundable credit amount. Remember, a refundable credit is one that actually has the IRS giving you money beyond just giving back tax that you overpaid. Jim and Pam already owed $0 of federal income taxes, and now are getting a refundable tax credit of $2,000. Here's how it breaks down:

And here's how it looks on the 1040:

$2,401?!

GLORIOUS.

In case you fell asleep somewhere in there (taxes seem to have that kind of effect), here's the bottom line: when Jim and Pam just categorized their pell grants as plain ole' tax-free scholarship, they got a $270 refund. All that meant was they were having returned to them money they overpaid through paycheck withholdings, because they only owed $141.

But after including their pell grants as income on purpose and maximizing the American Opportunity Tax Credit, they got $2,401 back.

THAT'S A DIFFERENCE OF $2,131 MORE MONEY IN THEIR POCKETS (INSTEAD OF THE IRS'S).

Be amazed for a few moments, then pick yo' jaw up off the floor. It's not a magic trick (sorry for the false advertising), just tax planning!

And what if this has happened the last couple years to Jim and Pam too but they filed their taxes the other (less "ka-ching") way? Well, you can amend your tax returns going back three calendar years only. Better hurry up and check...

DON'T TRY THIS AT HOME

Unless you feel well-versed in taxes and are confident that you can confirm your eligibility for the American Opportunity Tax Credit and that your pell grants (or other scholarships) fit the requirements to make this strategy work, don't try to do this yourself.

There are some ways that this can get complicated, like the timing of pell grants for one school year that span two different calendar years and when you paid the education expenses and all that.

Also, note that if you're trying to do this with scholarships that aren't pell grants, you have to make sure that the scholarship's terms are that you "must" or "may" apply the funds to things other than qualified education expenses like room & board, travel, etc. In other words, scholarships that have to be for qualified education expenses can't be included in gross income.

You also need to weight your net benefit of using this strategy. Why? Because raising your income intentionally to claim more of the American Opportunity Tax Credit means you have to report more income for other things, where the effect will be reduced benefits. Raising your AGI may decrease other tax deductions or credits, raise your state tax income, or make you eligible for less or no public benefits like state aid or other government programs. Oftentimes, the increased refund from this strategy is large enough for the net benefit to be worth it, but you need to consider everything.

So, as always, check with your qualified tax professional!...if you still trust them for missing a game-changer like this.

And if it hasn't hit you yet, this is why tax planning is such an important part of comprehensive financial advice - the tax law touches just about every large financial decision you make.

Have fun reaping the extra tax refunds!